10 Things Your Financial Advisor Won’t Tell You

If you’ve been keeping up with the news, you may have come across something about financial advisors. In case you missed it, here are the cliff notes: the Department of Labor (DoL) says financial advisors must be a fiduciary in some circumstances.

A fiduciary Financial Advisor is someone who must act in their client’s best interest. The DoL ruling may surprise some consumers who had assumed that their advisor was working in their best interest.

Unfortunately, the DoL ruling isn’t a panacea for your advisor keeping secrets from you. Because in addition to not telling you that they’re not working in your best interest, there are other things that your financial advisor won’t tell you. I’ve put together a list of some of the things your advisor may not be telling you – and what you can do about it!

Table of Contents

Top 10 Things Your Financial Advisor Won’t Tell You

- I Don’t Have Your Best Interest in Mind

- My Title Doesn’t Mean Anything

- I Get a Cut When You Buy a Financial Product

- Fee-BASED is a Meaningless Term

- The 4% Rule is Dead

- You’re Not Going to Get 20% Investment Returns

- Pre-Pay Your Debt

- Diversify Your Retirement Income

- You Should Delay Getting Social Security

- Annuitize Your Pension

#1 I Don’t Have Your Best Interest in Mind

Are you working with a salesperson masquerading as a financial planner? Unlike a fiduciary, a commissioned salesperson’s number one goal is to sell. It’s not to make sure that you’re getting the best financial advice to help you reach your goals.

The commissioned salesperson is under no obligation to make your life better. Their true incentive is to earn a commission from a sale. The bigger the commission, the bigger the incentive.

What’s the solution? Work with a financial advisor who has pledged themselves as a fiduciary.

#2 My Title Doesn’t Mean Anything

As John Oliver hilariously pointed out on Last Week Tonight, the following titles are meaningless:

- Financial Analyst

- Financial Consultant

- Financial Advisor

- Financial Planner

- Investment Consultant

- Wealth Manager

Anyone can call themselves any of the above.

So, what do you do if you’re looking for financial advice? Opt for a CERTFIED FINANCIAL PLANNERTM. Did you note the capitalization and TM at the end? That’s because the CFP® designation means something special. See how I did it again with the little “®”?

CFP® professionals must pass an array of requirements to be granted their designation, including:

- Education

- Experience

- Examination

- Ethics

#3 I Get a Cut When You Buy a Financial Product

If you’re working with a commissioned salesperson, they’re likely trying to sell you something. Why are they doing this? Why is it always,

- “you need to buy this life insurance to protect your family,” or

- “you need to buy this mutual fund to save for retirement,” or

- “you need to put money in this 529 to pay for college”

Does that make sense? How is it possible that every single financial problem has the same answer: buy a financial product?

Commissioned salespeople only make money when you buy something. Therefore, their “free” advice usually suggests you buy a financial product, like whole life insurance.

The solution to buy shouldn’t make sense; not every financial problem requires a purchase. Sometimes it’s the opposite. Readers of the personal finance blogs know well that sometimes the best option is to not spend money.

But, even if your financial problem was solvable via purchasing a financial product, the bad news is that the financial products offered by a commissioned salesperson are usually the worst financial products to buy.

Why do commissioned salespeople offer such terrible financial products? Because the salesperson’s commission is baked into the cost of the financial product.

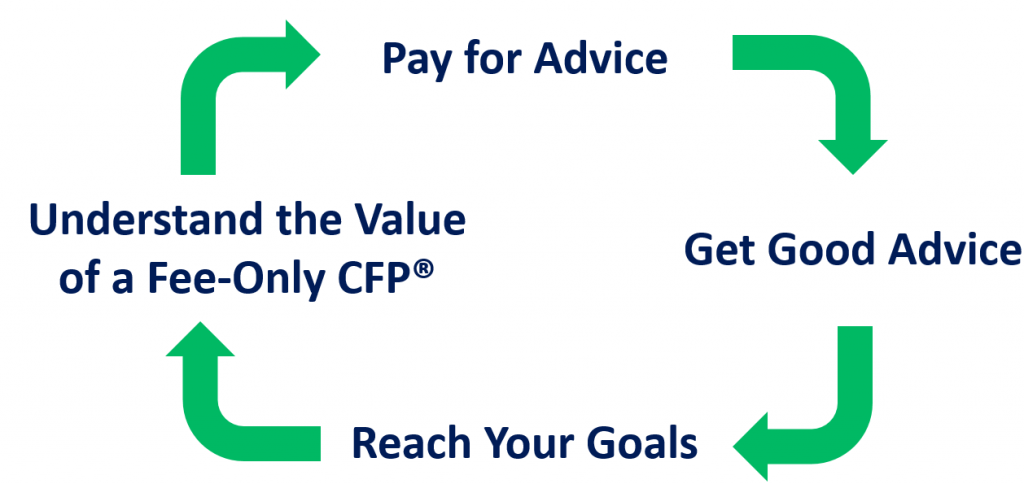

What’s the solution? Work with a fee-only CFP® professional! When you work with a fee-only professional, you pay for advice – and not for an overpriced financial product that you may not need.

#4 Fee-BASED is a Meaningless Term

You’ll notice that I just said, “work with a fee-only CFP® professional.” What I didn’t say is work with a fee-based advisor. What’s the difference? Only everything.

When you work with a fee-only advisor, you get someone who can never sell you any financial product. When you work with someone who is fee-based, they can just as easily sell you something. So, make sure to choose fee-only. Don’t fall for fee-based.

What a Fee-Only CFP® Fiduciary Won’t Tell You

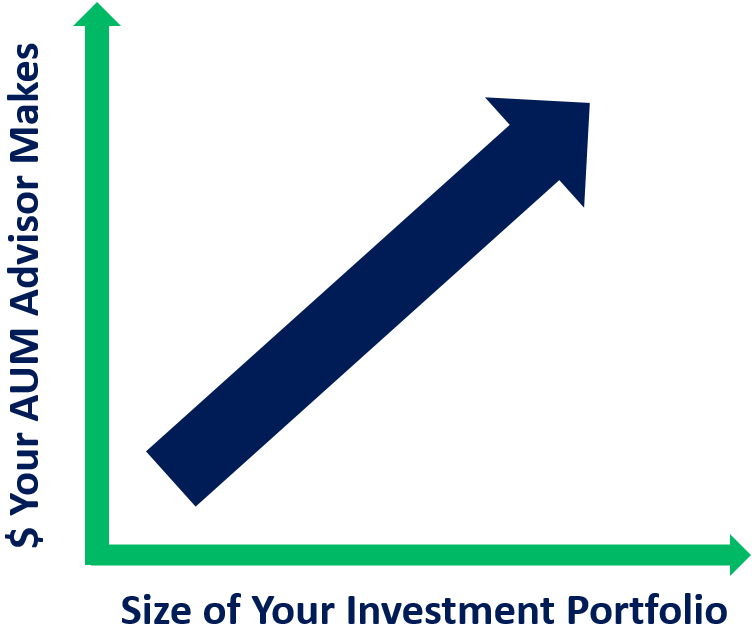

So far, I’ve advocated for patronizing a fee-only CFP® professional. But, even a fee-only CFP® professional has a conflict of interest if they’re offering an assets under management (AUM) investing service.

If you’re not familiar with AUM billing, think of an online automated investment service (AKA a robo-advisor). You put in $5,000 – and the robo-advisor takes their 0.25% of your money. If your portfolio grows in value, the robo-advisor makes even more money. If your portfolio declines in value, they make less money. This puts you and the AUM advisor on the same page: you both want the portfolio to get bigger – not smaller. When the portfolio gets bigger, you both make more money.

The percent of assets is a good start in aligning client and advisor interest. But, it’s not perfect. To prove it, here are some things that even your fee-only advisor won’t tell you.

#5 The 4% Rule is Dead

I love the early retirement movement! It is truly inspiring. I too long for the chance to live on a large piece of land (where I can adopt all the rescue foster dogs).

But, I cringe when I see early retirement bloggers talking about the 4% rule. Why? Because the 4% rule is a thing of the past. If you think your investment portfolio can sustain a 4% withdrawal every year, think again. Here’s why:

- In his study, William Bengen’s 4% rule was applied to a 60-year old retiree. Bengen didn’t do an analysis past 50 years of withdrawals. If you’re planning on retiring at 30 or 40 and living to age 100, you very likely may run out of money using the 4% rule.

- Bengen’s research was published in October of 1994. Newer studies have declared sustainable withdrawals rates can be as low as 1.26% net of fees, depending on your allocation.

Yet, if you’re an advisor offering investment management services, being honest with clients about investment returns may mean turning off potential customers.

SPONSORED WISERADVISOR

Choosing the right financial advisor is daunting, especially when there are thousands of financial advisors near you. We make it easy by matching you to vetted advisors that meet your unique needs. Matched advisors are all registered with FINRA/SEC. Click to compare vetted advisors now.

#6 You’re Not Going to Get 20% Investment Returns

Marketing a 20% investment return is a good way to get money in the door. But, just like sustaining a 4% withdrawal rate is not possible, neither are outsized investment returns. If you hear about investment returns that seem too good to be true, they probably are.

#7 Pre-Pay Your Debt

The advisor charging for a percent of assets wants your investment portfolio to be as big as possible – so he can get paid as much as possible. This means the advisor may advise you to keep more of your money invested in the stock market – and under their management.

Sometimes it may make sense to pre-pay your debt. It depends on a myriad of things, like risk tolerance, investment allocation, the term and interest rate of the debt. However, the conflict of interest that stems from an AUM advisor means you’re likely to be encouraged to carry debt so as to keep your AUM portfolio as large as possible.

#8 Diversify Your Retirement Income

The stock market is a great way to invest – but it’s not the only way to make money. There is also rental property. Rental property is a very different type of investment compared to the stock market. It has its own unique challenges. But, just as you diversify your portfolio with different stocks, you should also diversify your retirement income. Consider rental property, part-time employment, hobby income, or a small business venture as a way to supplement your (early) retirement income.

However, the investment advisor charging a percent of assets won’t tell you this. Why? Because putting money into real estate (or anything else) means that money has to come from somewhere – and if that money comes from the investment portfolio managed by the advisor, that means less money for the AUM advisor.

#9 You Should Delay Getting Social Security

Delaying Social Security means getting a guaranteed 8% investment return on your Social Security payment. You won’t see a guaranteed rate like that anywhere else – except maybe government bonds of the 1980’s. (But unless you have a time machine, you can’t buy those.) If you’re delaying receiving Social Security, money to fund your living expenses must come from somewhere. And that means it’s coming from your investment portfolio.

An advisor charging a percent of assets under management (AUM) will likely tell you to take Social Security now. And it’s bad advice (because you’d be giving up an 8% guaranteed investment return).

#10 Annuitize Your Pension

Fee-only CFP® fiduciaries and celebrity consumer experts alike will tell you to avoid buying an annuity. But I’m talking about a different kind of annuity here: annuitizing your pension.

You’re given an option on how to claim that. There are normally at least a couple options:

- Annuitize your pension – entitling you to monthly income for life, or

- Get a one-time lump-sum distribution

Sometimes it makes sense to choose one option over the other. There are lots of considerations, such as:

- Your life expectancy

- The rate of investment return available with other investments (opportunity cost)

- Your needs for liquidity (to be able to get at all the money instead of just the monthly payment)

- The financial strength of the pension / company providing the pension

The choice to annuitize a pension is a very personal decision. There is no one-size-fits-all answer. But, the financial advisor almost has the same answer: take the lump-sum distribution. Why does the financial advisor want you to take the money and run? Because having a client get a big chunk of cash means the advisor has a chance to get a piece of cash from:

- Getting a commission on selling life insurance

- Getting a commission from selling a mutual fund

- Getting a bigger assets under management fee for investment management

The Future of Financial Planning

The Department of Labor rulings are a good start – but there are still many conflicts of interest in the industry.

How do you get the best possible advice from a financial advisor? Find a financial advisor who

- pledged themselves as a fiduciary

- is a CFP® professional

- is fee-only

Lastly, skip the AUM billing model. Instead, choose a fee-only CFP® professional pledged as a fiduciary who charges via:

- An hourly rate (i.e. $250/hour)

- An on-going monthly retainer (i.e. $100/month)

- A one-time retainer fee for a financial plan (i.e. $3,500 for a six-month contract)

These options set up the client to receive the best advice possible with the least possible conflicts of interest. And, when you work with a fee-only CFP® fiduciary charging on a retainer or hourly basis, there is much less you don’t have to worry about your advisor not telling you.