Should You Hold Or Sell Your Long-Term U.S. Government Bonds?

The Pandemic and the ensuing Fed actions to revive the market by easing liquidity has pushed the yield of the benchmark 10-year Treasury bonds to near record lows; yield as of October 2020 is at a measly 0.7%. Meanwhile, the price of the bonds in the open markets surged due to their inverse correlation to the yield, tempting investors to sell their bond holdings. With the Fed vowing to pin its interest rate near zero until at least 2023, it becomes essential for us to understand, rethink, and replan one’s bond investment options. The following information is to help you get a better understanding and reach an informed decision regarding your portfolio holdings of U.S. Government Bonds.

Table of Contents

1. Understanding Bonds

a. What are government bonds?

A government bond is a debt-based investment, where you’re basically loaning your money to the federal government. In return, you get periodic interest at a predetermined rate and the promise of repayment of the bond’s face value on the maturity date. The government utilizes the money raised to fund projects and infrastructure.

b. How do government bonds work?

When you invest in sovereign bonds, you lend the government a certain sum on which you are paid a set rate of interest at regular intervals. This interest, fixed during issuance, is known as a Coupon. This kind of investment makes bonds fixed assets. The bond price (principle or market value) fluctuates with market mechanics. At the end of the maturity period of the bond, the government will repay the price value of the bond.

Different bonds have different maturity periods. Depending on the type of bond you buy, the maturity period can vary from within a year to over 30 years.

Similar to shares, bonds can either be held for a long time or be sold in the open market. A lot of factors affect the prices of the bonds. Some of these are supply and demand (Governments can supply bonds on a need-basis). The demand for a bond depends on how promising the returns are, credit ratings, and how close are the bonds to maturity.

Treasury bonds, also known as T-bonds or T-bills, are bonds that expire in more than ten years. They are considered to be the safest among government bonds.

c. Risks associated with bonds

Government bonds, in general, have an image of being the safest investment option. However, the investment scenario is more complicated than just that. Government bonds are not risk-free investments. Frankly, no investment is risk-free. There are several risks associated with government bonds too, and one should always remember that ultimately, government bonds are governed by the market forces.

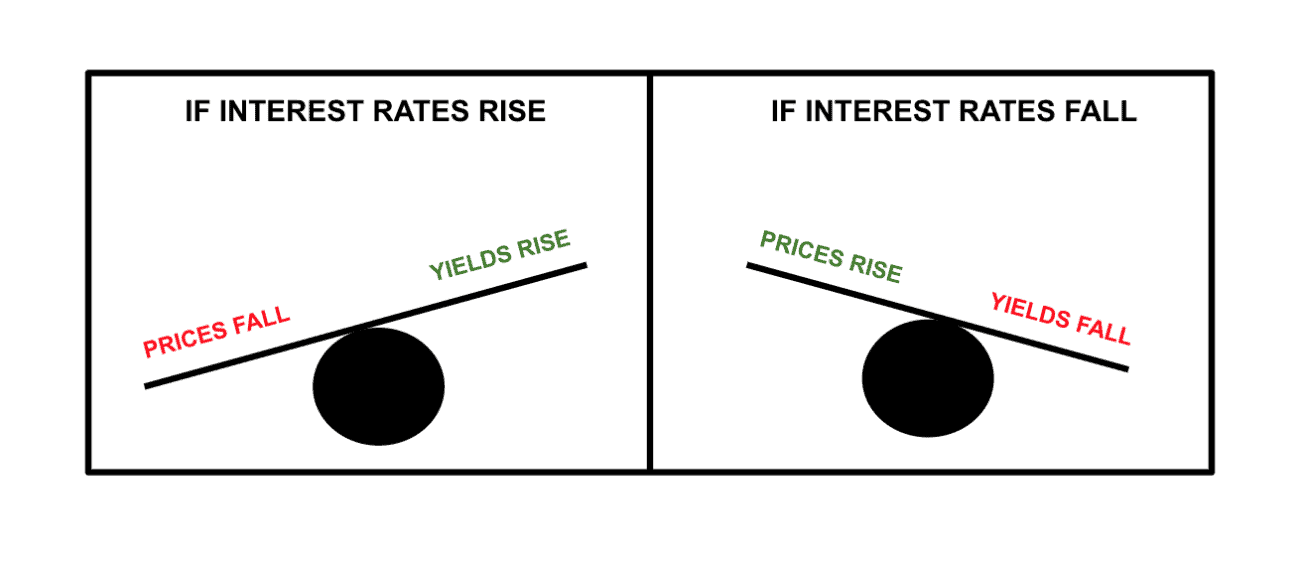

One such risk associated with these bonds is interest rate risk. There is a possibility that with a rising rate of interest, potential investors will no longer find the fixed lower interest bonds attractive, resulting in a lower market value of the bond.

Another risk is from inflation. Rising inflation makes the value of bonds take a dive.

Then there is, of course, the currency risk. On the flip side, currency value appreciation could offset a low yield for international investors, but this is highly risky, as future prediction of currency movements is tricky.

Some say that holding government bonds right now might not be in the investor’s favor, given the risks associated with it.

d. Advantages of investing in government bonds

What makes bonds a good investment option, and whom are they meant for? Bonds could be an excellent fit for someone looking for safer investment avenues. While no investment is risk-free, government bonds are not subject to the volatility of market conditions such as equities, and hence, have a reputation for being the de-facto safe investment option.

T-bonds are considered the safest investment in the world because they come backed by the ‘full faith and credit’ of the U.S. government. Since it is almost impossible to imagine a breakdown of the ‘greatest economy in the world’, T-bonds present as an alluring investment option. Ratings agencies such as Fitch and Moody’s have also assigned T-bonds an AAA rating, the highest in the world, which is further indicative of their safety.

If your portfolio already has exposure to investment in stocks, then T-bonds may be a good diversification option to buffer against the high-risk shares.

Another advantage is that the income from T-bonds is received in the form of interest. The nearly guaranteed income is stable and secure, thus making it a favorite for those seeking regular payouts. If the bonds are held until maturity, the investor receives the entire principal back too. Thus, the investment is never lost unless the government defaults, which is far-fetched for strong economies such as the United States. The U.S. government has never defaulted on a debt or missed payment on debt till date.

In some instances, an investor can capitalize on the resale of the bonds. At times, bond traders may bid the price up of the bond in the open market beyond the bond’s face value, fetching investors a handsome profit.

Another important advantage of T-bonds is their liquidity. The market for Treasuries is large and active, making it relatively easy to buy or sell Treasury bonds, notes, or bills in various quantities and maturities.

e. Disadvantages of investing in government bonds

Now that we have gone through the advantages of investing in government bonds, let us explore some disadvantages of holding this security to help you make informed decisions.

Firstly, bonds are a low-yield investment because the risks associated with these bonds are low, and therefore, have low returns. In investing parlance, this is called an opportunity risk – where the money locked in this investment could have earned you a higher return had it been invested in some other asset. In contrast, corporate bonds and shares have a higher rate of return.

Treasury bonds are also subject to many of the risks associated with fixed income instruments – primarily, that of interest rates. As interest rates go up, Treasury prices in the market go down as the product may no longer be attractive to investors (investors will pump money into products that yield higher returns). Inversely, if interest rates go down, that translates into lower yield returns, even though market prices may then be going up as investors may find it affordable.

Generally, the longer the maturity of the Treasury security, the more significant is the drop in market price. This means that Treasury bonds are most affected by interest rate risk, while treasury notes have somewhat lesser risk, and bills, with their shorter-term maturity, have the least exposure to interest rate risk.

This also brings to light the fact that bonds have a longer gestation period (time to maturity) than other financial instruments. Some bonds can make you wait as long as 30 years!

An investor should also take note of inflation that could affect the returns from bond investments. It could negate interest or even eat into savings. Additionally, while there are no local or state taxes levied on the bonds, you might have to pay federal tax on this type of investment.

Some treasury bonds have ‘call provisions’ that allows the government to retire them before the originally-stated maturity date. The government can take this action when rates fall beyond conducive limits.

SPONSORED WISERADVISOR

Choosing the right financial advisor is daunting, especially when there are thousands of financial advisors near you. We make it easy by matching you to vetted advisors that meet your unique needs. Matched advisors are all registered with FINRA/SEC. Click to compare vetted advisors now.

COVID-19 —while posing a severe threat to public health—has also disrupted the economy and financial markets, prompting a strong desire among investors for safer and liquid investments. In such a situation, one might expect U.S. Treasury bonds to be the investment of choice, but for a while in March 2020, the $18 trillion U.S. market saw some loosening of investor interest. Despite the very volatile stock market, led by extremely low interest rates, bonds failed to attract investors as much as expected.

What caused the volatility?

The U.S. Treasury bonds market is quite deep and highly liquid. This means that investors can buy and sell large quantities of these securities without affecting the market price of the bond. Market participants—banks, insurance companies, asset managers, mutual funds, and others—rely on this easy selling-ability of their bond holdings to meet their demand for cash. However, in March 2020, when the markets met the challenging and damaging impact of COVID-19, investors gave up Treasuries in a rush in order to get cash. In some cases, this was a reflection of their investment objectives—selling Bonds in order to buy depressed equities. In other cases, these sales were forced by losses or the need to settle short-term debts, and the market proved unable to handle the surge in Treasury sales.

The lesson learned: No investment is risk-proof. Bonds’ depth and liquidity were gone, prices became extremely volatile, and sellers could not find ready buyers at a reasonable price. The uncertainties and such a large-scale industry deleveraging only furthered the downturn.

4. Should you continue to hold bonds in the future?

The current interest rates are lower than the historical averages. It is imperative to mention here that the historical average return may not be very relevant for someone looking to estimate future market returns. Investing mogul, Warren Buffet, has often warned investors about this false fascination with the past. He calls it a recipe for disaster. The problem with attempting to gain insights from historical outcomes is that future market returns are connected to the current values rather than their historical performance.

Returns on bonds are dependent on initial bond yield and subsequent yield changes. Low bond yields will translate into lower returns, and the heightened interest rate risk associated with capital losses when interest rates rise needs to be kept in sight.

The 2020 yield curve inversion began on 14 February 2020. The yield on the 10-year note fell to 1.59%, while the yield on the one-month and two-month bills rose to 1.60%. Investors were growing concerned about COVID-19.

The inversion worsened as the situation got grimmer. Investors rushed to sell the bonds, and yields fell, setting new record lows along the way. By 9 March 2020, the 10-year note had fallen to a record low of 0.54%. The yield on the one-month bill was slightly higher, at 0.57%. Additionally, there are ongoing pressures to keep yields low.

5. Conclusion

America is undergoing a major transition – economically and politically. Add to the mix that government machinery all across the world was on a standstill with lockdown imposed to combat COVID-19, we are yet to assess the actual impact to business and sentiment. There is no denying that GDP (gross domestic product – the measure of growth of an economy) is affected and may remain subdued for the coming few years.

The Fed is doing everything possible in its power to buoy the economy and keep it from receding into a depression from the current recession-like situation by releasing stimuli packages for the economy. In the light of these efforts, it remains for us to consider how government programs affect the value of money and what investments become attractive.

It is true that interest rates are languishing near all-time lows with no signs of a revival at least in the near-term. Will it make sense to purchase bonds at this low rate of return? On the other side of the coin, government bonds continue to be the safest investment options. Popular opinion is that given the unpredictable social, political, and economic circumstances, it might be a good idea to continue to hold the currently high-priced bonds. However, it may not be a good idea to trade off shares for bonds. The current environment calls for bonds to be a fallback option and not your mainstream portfolio component.

If you are still confused about whether you should hold or sell your bonds, and need guidance, you can get in touch with a professional financial advisor using the free match tool on Paladin Registry! The fiduciaries on the platform can provide you with the necessary personalised guidance and assist you to reach your financial goals.

To learn more about the most suitable tax-saving strategies for your specific financial requirements, visit Dash Investments or email me directly at dash@dashinvestments.com.

About Dash Investments

Dash Investments is privately owned by Jonathan Dash and is an independent investment advisory firm, managing private client accounts for individuals and families across America. As a Registered Investment Advisor (RIA) firm with the SEC, they are fiduciaries who put clients’ interests ahead of everything else.

Dash Investments offers a full range of investment advisory and financial services, which are tailored to each client’s unique needs providing institutional-caliber money management services that are based upon a solid, proven research approach. Additionally, each client receives comprehensive financial planning to ensure they are moving toward their financial goals. CEO & Chief Investment Officer Jonathan Dash has been covered in major business publications such as Barron’s, The Wall Street Journal, and The New York Times as a leader in the investment industry with a track record of creating value for his firm’s clients.

Other posts from Jonathan Dash