What is an inverted yield curve, and what does it mean to me?

Gary Williams

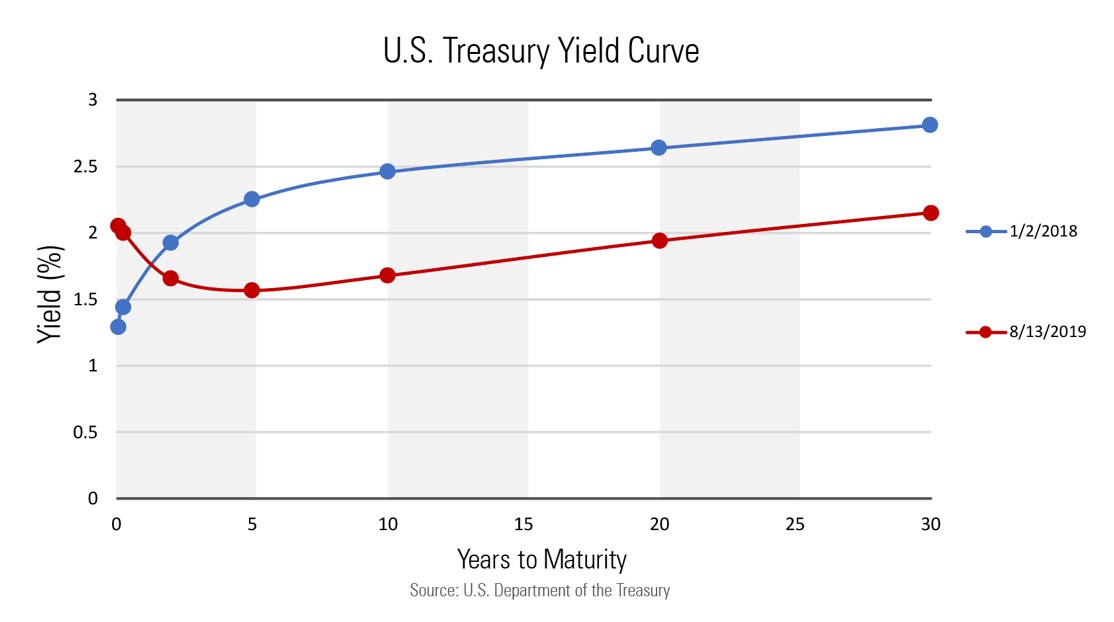

Inverted-Yield-Curve

In early August of 2019, headlines referring to the feared “inverted yield curve” were on display all over news, financial websites and publications, sparking a more than 2.9% decline in the S&P 500 (Source: Yahoo Finance), its worst single-day of trading for the year. The following day, a plethora of articles were published explaining an inverted yield curve and linking its direct correlation to an imminent recession, further weakening investor sentiment. In this day and age where the headlines are often times scary, many are wondering: what is an inverted yield curve and should they panic?

Table of Contents

Why is the inverted yield curve important?

An inverted yield curve simply occurs when shorter-term interest rates are higher than longer-term rates. A good way to understand this is using an example of certificate of deposits (CD’s). If you purchase a six-month CD, you would expect the interest rate would be less than a three-year CD. However, when the yield curve inverts it, the shorter-term CD is earning a higher interest than the longer-term. This situation, which rarely occurs, has historically been a dependable indicator of a recession. On average, a recession occurs 18 months after the yield curve inverts.

Why does the yield curve invert?

At the short end of the curve, the Fed exercises direct control by raising and lowering the federal funds rate. The long end of the yield curve gets complicated, though, as it is influenced by investors’ expectations, specifically market sentiment and inflation expectations. Generally speaking, if investors believe the economy is going to face headwinds in the future, they will purchase longer term bonds which will cause longer-term interest rates to decline.

Should I be concerned about the inverted yield curve?

So, because you are now familiar with what an inverted yield curve is, now comes the question you are really wondering; what effect will an inverted yield curve have on my investments? There isn’t a simple answer, but historical data shows us that the results aren’t nearly as gloomy as media outlet headlines would lead you to believe. Let’s say the inverted yield curve does lead to a recession sometime in the next 12-24 months, would it be wise to move all your investments to cash? Gold? Under your mattress? The answer is most likely no. During the last 14 recessions in the U.S., stocks returned on average +1.2% while U.S. bonds returned +8.2% (Source: Morningstar). However, it’s important to note that these returns could have been much worse if an investor wasn’t properly diversified.

What tips should I follow in dealing with the inverted yield curve?